We live in an increasingly complex, fast moving and changing world – that’s immediately apparent. And there is an increasing body of writing about the characteristics of organisations designed to make the most of opportunities in that world (for example, Exponential Organisations). But, perhaps because it is still early days for traditional, global and multi-national organisations to come to grips with that VUCA world, there are comparatively few case studies about what those types of organisations can do to make the change, and perhaps more importantly just what it is that stops them.

Having seen many organisations in my working life, and thinking from my foresight perspective and how the trends and shifts play out, here’s what I’ve observed – no right answers but perhaps some provocations.

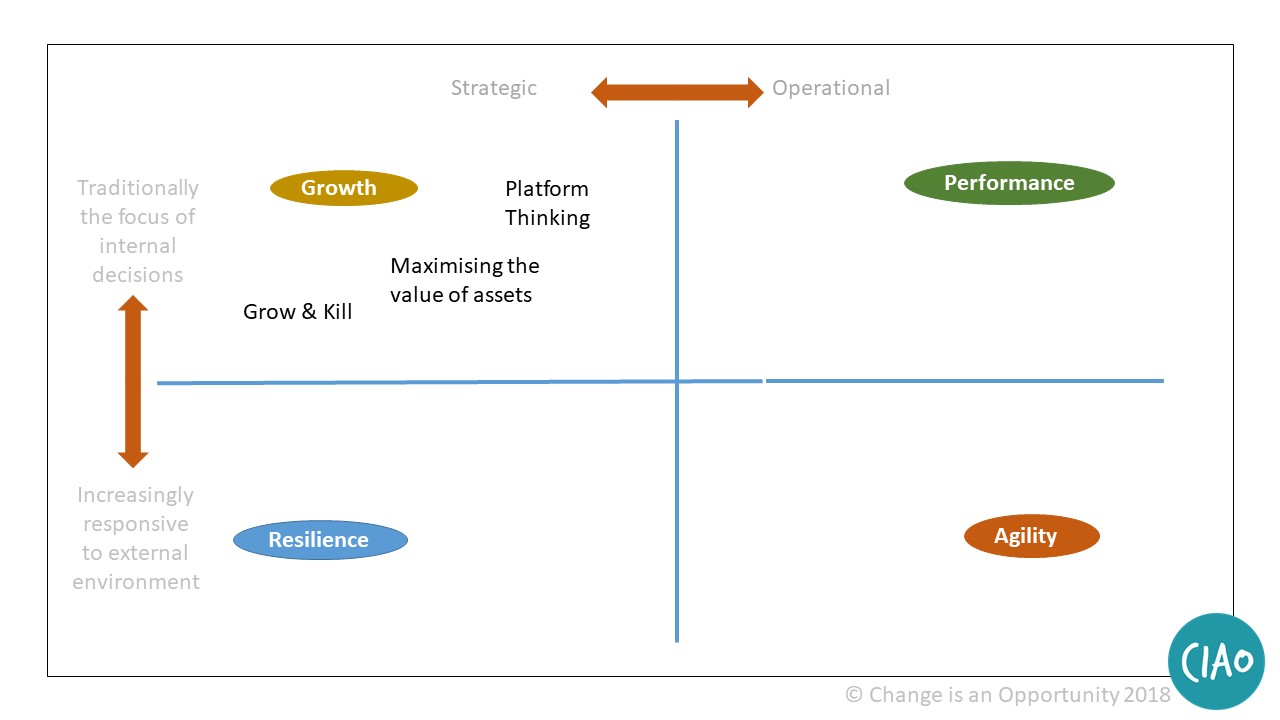

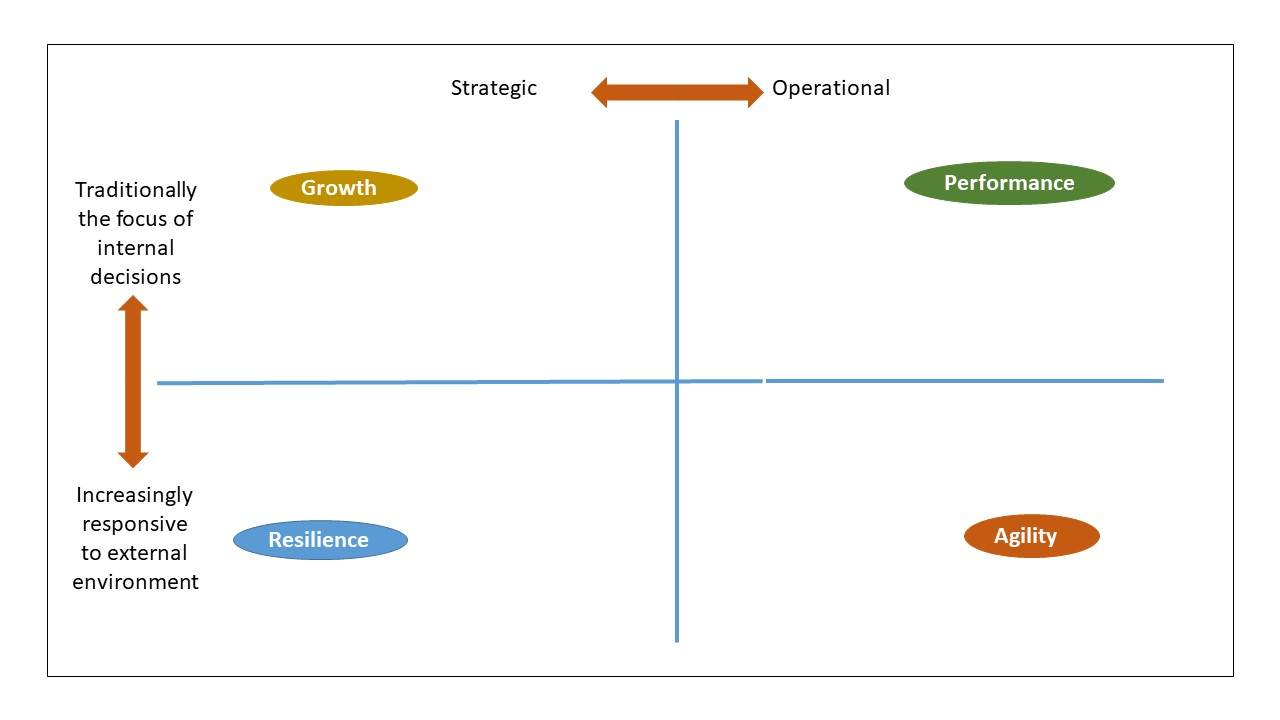

At the highest level, looking at the priorities of traditional organisations they have primarily been driven around 2 – performance (in the short and medium term) and growth (in the longer term). The perspective on both has almost invariably been internal – certainly in terms of action taken to drive them.

In the complex world of today, it seems to me there are two big changes to this:

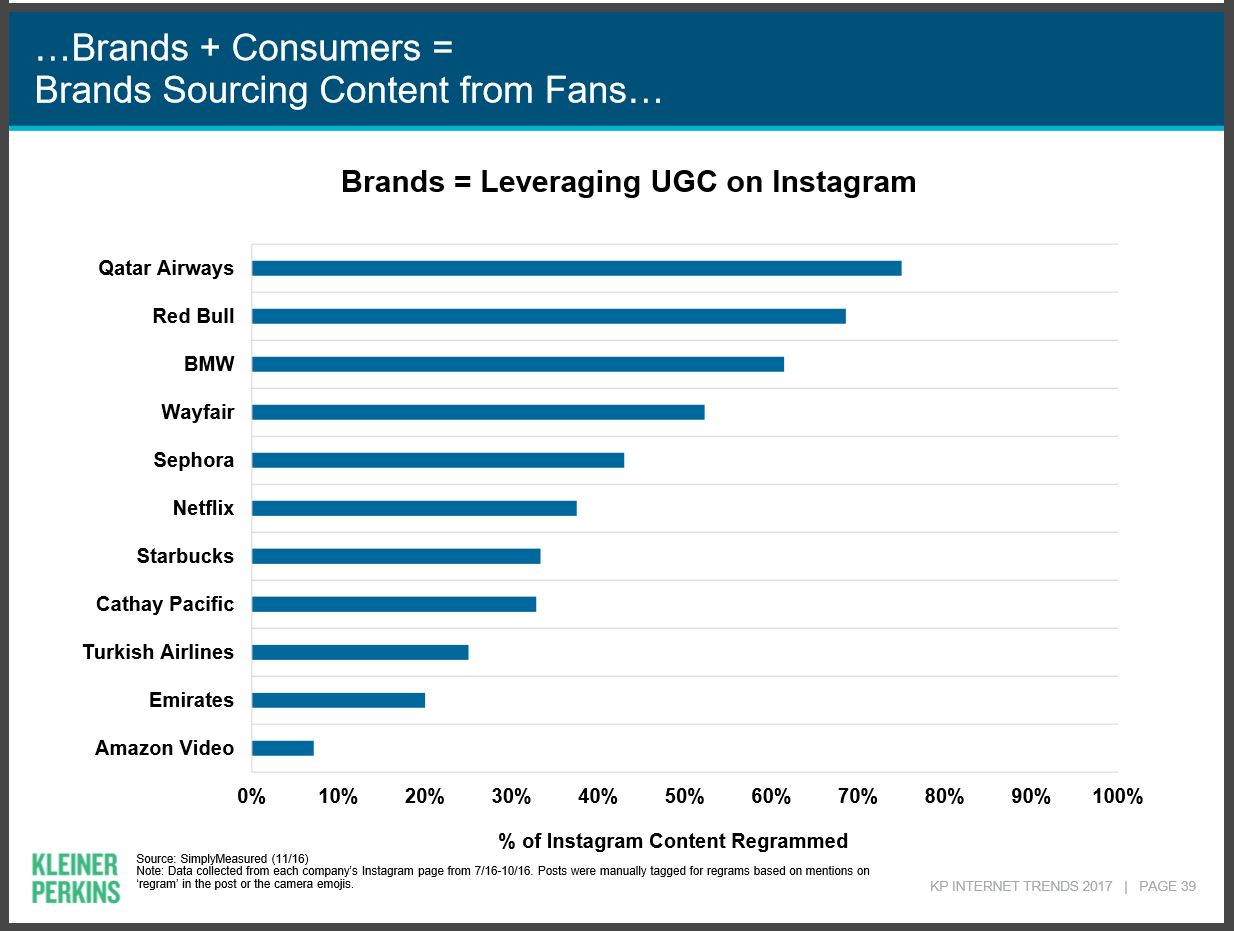

- Performance and growth still matter as much as ever, but the range of options to drive both has grown hugely – and in many cases require leadership to engage outside as much as inside. For example tactics like using User Generated Content (UGC) for marketing is less about the level of marketing department resources and more about the quality and nature of customer engagement – which will not be wholly within the control of the organisation at all.

Source: Kleiner Perkins – Mary Meeker Internet Trends 2017

- The need to add 2 further metrics of success in terms of agility (short and medium term) and resilience (longer term). The latter is not simply a question of financial resilience which it could be argued has always been a consideration but resilience of the business model, even of the organisation and its market niche. Both resilience and agility again require an external lens to be thoroughly understood – indeed it could be argued that the catalyst and drivers for both start externally.

Source: Change is an Opportunity Ltd

Source: Change is an Opportunity Ltd

And yet – how many organisations are designed and managed to prioritise the external context rather than the internal structure? Think of the nature of the Executive – CFO, COO, Head of HR perhaps – almost all key leadership roles are about the internal resources, disciplines and activities. I’ve mentioned this before in my post on Leading in an externally focused world.

I know when I run a foresight presentation how often the comment is made by the leadership team that they know they need to spend more time on thinking about what the world of the future looks like, but it clearly isn’t any one person’s responsibility and each is taken up with their own urgencies and pressures – so in these situations the net result is that it is constantly de-prioritised by all of them. Similarly the trends which superficially bear no relationship to the established business model are considered frequently with a detached view – interesting but, not yet at least, relevant to today’s business priorities. It seems that the concept that disruption comes from the unknown, not the known direction, is understood in theory only.

Additionally it’s clear that the necessary response to many of the trends doesn’t fall neatly into Finance, Procurement, Sales, Operations etc (perhaps not surprisingly as the external world isn’t organised like that). The barriers then are not simply time pressure or misunderstanding but structural in nature.

Those organisations best placed to engage with all 4 success criteria of growth, performance, agility and resilience are those that have recognised (amongst many other aspects) the need for:

- A continuing informed external perspective made available across the organisation. A truly impactful leader I met headed their organisation’s Competitive Intelligence division – and used his regular slot at their Executive to challenge the conventional and current view of their future operating environment but in a neat way that meshed with their existing approaches whilst provoking new thinking.

- Cross-disciplinary decision making groups. The most common instance of this today is in innovation where multi-functional groups with diverse members are increasingly applied – but in reality why limit this purely to innovation?

- The ability to demonstrate rather than tell the organisation how relevant and immediate a disruptive trend is, together with it’s potential impact on the established model – whether this is in creating an app to change perceptions of how customers could interact or the more dramatic ‘speedboat’ intrapreneur groups aiming to cannabalise the core business as at Aviva’s innovation garages.

More to follow