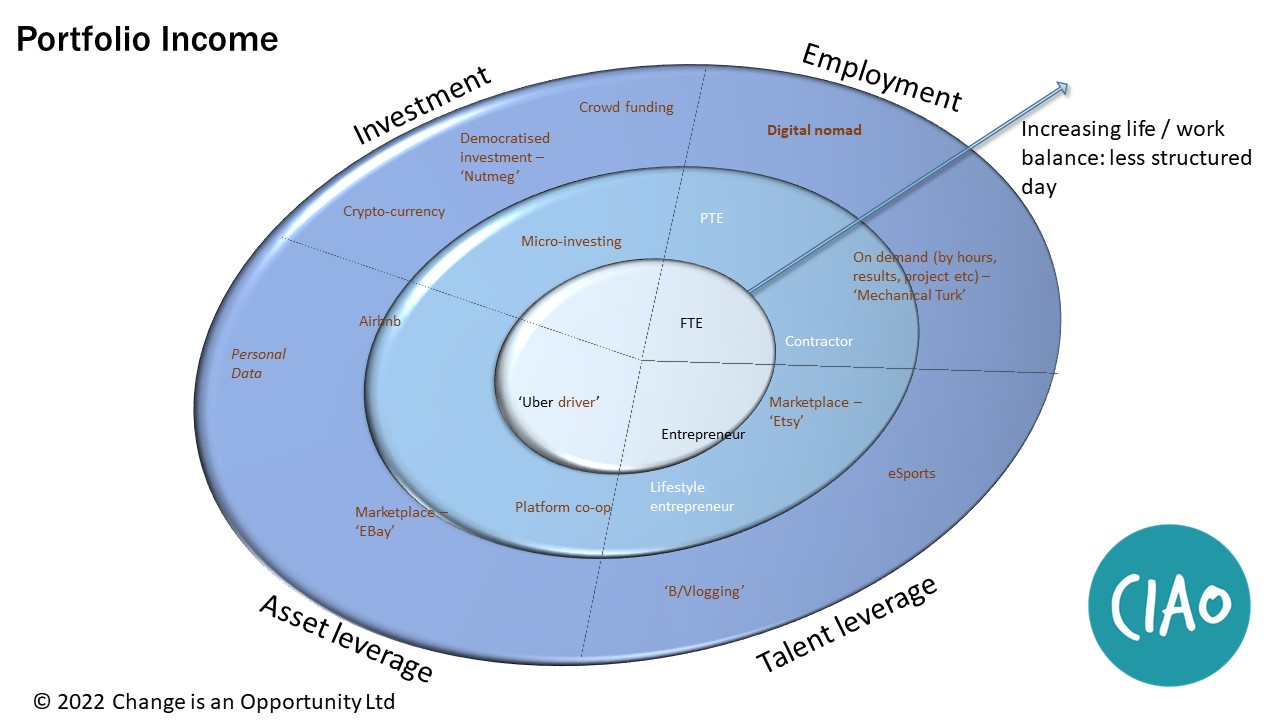

Well the question of tax, and how much of the newer forms of income are identified is already an issue. Some trading on eBay will inevitably hit UK capital gains thresholds but not all by any means. Airbnb rentals are absolutely akin to historic house rentals but if the owner provides (and charges for) additional services like a guided tour of the locality, cooking demonstrations, language teaching – does this become more of a formal business? The lines of distinction between business / personal; capital/income; incidental / regular will become significantly harder to define if portfolio income takes off.

And that’s before the question of where this activity will take place. Digital nomads were, at least until Covid interrupted, becoming more common. As more of our lives become virtual the question of where an activity is genuinely taking place becomes greyer. If a 3D print design is created by someone in the UK, but only drives revenue when it is used to print the item in say, USA – how does that work?

And above all there is the shift in mindset needed here. If portfolio income becomes the norm, then so many of our fundamental assumptions about the relationship between work and income will need to shift – where, who, how, what time of day, how the income is defined . . . . the list is endless. And will the complexity of these arrangements be left to the individual to sort out? Or will government need to educate, enable, facilitate and support – if for no other reason than to ensure equality of opportunity?

I’m quite sure that isn’t a definite list – more the tip of the iceberg. And I think there are many more new opportunities to come. So watch this space!